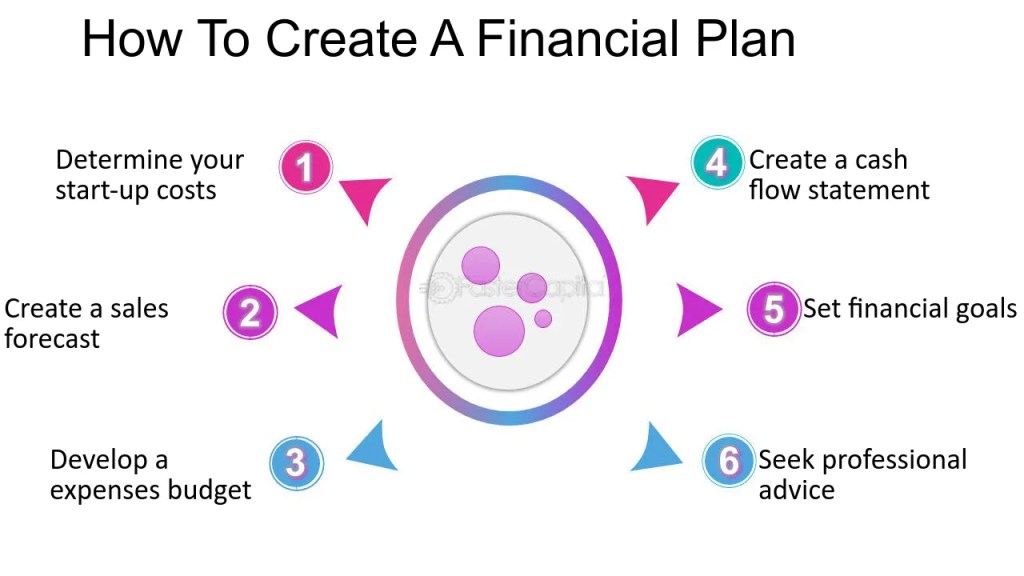

In today’s digital age, online fraud is a growing concern for individuals and businesses alike. As technology evolves, so do the tactics employed by scammers, making it increasingly difficult to identify and protect oneself from fraudulent schemes. The internet offers numerous opportunities for scammers to exploit unsuspecting victims, from phishing emails and identity theft to fake websites and investment scams. Therefore, it is crucial to take proactive steps to protect yourself from online fraud. This article will explore the best practices for online fraud prevention, providing practical tips on how to stay one step ahead of scammers.

Understanding Online Fraud

Online fraud refers to any deceptive activity that occurs over the internet with the intent to defraud individuals or organizations. Scammers often use sophisticated techniques to manipulate people into providing sensitive information, such as passwords, credit card numbers, or social security numbers. Some of the most common types of online fraud include:

- Phishing: Fraudulent emails or websites designed to impersonate legitimate institutions, such as banks or e-commerce platforms, in order to steal personal information.

- Identity Theft: Scammers collect personal information and use it to commit fraud, such as opening credit accounts or making unauthorized transactions in the victim’s name.

- Investment Scams: Fraudsters offer fake investment opportunities, such as cryptocurrency schemes or high-return stocks, to trick victims into parting with their money.

- Online Shopping Scams: Fake online stores or auction sites that lure consumers into making purchases for items that never arrive.

With these risks in mind, it is essential to adopt a comprehensive approach to online fraud prevention that includes awareness, technological tools, and proactive measures.

Key Strategies for Online Fraud Prevention

1. Use Strong, Unique Passwords

One of the simplest and most effective ways to prevent online fraud is by using strong and unique passwords for all of your online accounts. Weak passwords, such as “password123” or “qwerty,” are easily guessed by hackers, allowing them to gain access to your accounts. A strong password should be a combination of uppercase and lowercase letters, numbers, and special characters. Avoid using easily identifiable information, such as birthdays or names, in your passwords.

Furthermore, it’s essential to use different passwords for each of your accounts. If a hacker gains access to one of your accounts, they will not be able to use the same password to access your other accounts. Consider using a password manager to securely store and generate strong passwords for all of your online accounts.

2. Enable Two-Factor Authentication (2FA)

Two-factor authentication (2FA) is an additional layer of security that can help prevent unauthorized access to your accounts. With 2FA, even if a scammer has your password, they will not be able to log in without a second form of verification. This can include a text message with a code, an email verification, or a biometric scan, such as fingerprint or face recognition.

Many online services, including email providers, banking platforms, and social media sites, offer 2FA as an optional feature. Enabling 2FA is a simple yet effective way to enhance the security of your accounts and significantly reduce the risk of online fraud.

3. Be Cautious of Phishing Scams

Phishing is one of the most common forms of online fraud. Scammers often send fraudulent emails or text messages that appear to come from legitimate sources, such as banks, government agencies, or online retailers. These messages typically ask you to click on a link, download an attachment, or enter your personal information on a fake website.

To avoid falling victim to phishing scams, always verify the sender’s email address or phone number before responding to any messages. Be cautious of any unsolicited requests for personal information, especially if they involve urgent or alarming messages. A legitimate organization will never ask you to provide sensitive details through email or text. When in doubt, contact the organization directly using their official contact information.

4. Monitor Your Financial Accounts Regularly

Regularly monitoring your financial accounts is crucial for identifying signs of online fraud. Check your bank statements, credit card statements, and credit reports for any unauthorized transactions or changes to your accounts. Many banks and financial institutions offer fraud detection services that can alert you to suspicious activity in real-time.

In addition, consider using services that allow you to freeze your credit or place fraud alerts on your credit file. This makes it more difficult for scammers to open accounts in your name or take out loans using your identity.

5. Invest in Anti-Malware and Anti-Virus Software

Malware and viruses are common tools used by scammers to gain access to personal information. These malicious programs can infect your computer or mobile device, recording your keystrokes, capturing screenshots, or monitoring your browsing activity. To prevent malware infections, always use reputable anti-virus and anti-malware software. Ensure that your software is updated regularly to protect against new threats.

Additionally, avoid downloading software or opening email attachments from untrusted sources. If you need to download files or software, make sure you are doing so from official websites or trusted platforms.

6. Be Mindful of Public Wi-Fi Networks

Public Wi-Fi networks, such as those found in cafes, airports, or hotels, can be a prime target for hackers looking to intercept your personal information. When using public Wi-Fi, avoid accessing sensitive accounts or entering personal information, as the network may not be secure. If you must use public Wi-Fi, consider using a Virtual Private Network (VPN) to encrypt your internet connection and protect your data.

7. Report Suspicious Activity Immediately

If you suspect that you have fallen victim to online fraud, it is crucial to act quickly. Report the incident to the appropriate authorities, such as your bank, the local police, or a national fraud prevention organization. The faster you report the scam, the better the chances of recovering your funds or preventing further damage.

Conclusion

Online fraud is an ever-present threat, but with the right precautions and awareness, you can significantly reduce the risk of falling victim to scams. By following the best practices outlined in this article, such as using strong passwords, enabling two-factor authentication, and staying vigilant against phishing attacks, you can protect yourself and your personal information from fraudulent activity. With the right tools and proactive strategies, online fraud prevention is within reach for everyone. Staying one step ahead of scammers requires a combination of knowledge, technology, and common sense—ensure that you are doing everything you can to safeguard your digital life. Visit RadleyFinance.com for More Information and assistance.